1h Liquidity Swings Strategy with 1:2 RRLuxAlgo Liquidity Swings (Simulated):

Uses ta.pivothigh and ta.pivotlow to detect 1h swing highs (resistance) and swing lows (support).

The lookback parameter (default 5) controls swing point sensitivity.

Entry Logic:

Long: Uptrend, price crosses above 1h swing low (ta.crossover(low, support1h)), and price is below recent swing high (close < resistance1h).

Short: Downtrend, price crosses below 1h swing high (ta.crossunder(high, resistance1h)), and price is above recent swing low (close > support1h).

Take Profit (1:2 Risk-Reward):

Risk:

Long: risk = entryPrice - initialStopLoss.

Short: risk = initialStopLoss - entryPrice.

Take-profit price:

Long: takeProfitPrice = entryPrice + 2 * risk.

Short: takeProfitPrice = entryPrice - 2 * risk.

Set via strategy.exit’s limit parameter.

Stop-Loss:

Initial Stop-Loss:

Long: slLong = support1h * (1 - stopLossBuffer / 100).

Short: slShort = resistance1h * (1 + stopLossBuffer / 100).

Breakout Stop-Loss:

Long: close < support1h.

Short: close > resistance1h.

Managed via strategy.exit’s stop parameter.

Visualization:

Plots:

50-period SMA (trendMA, blue solid line).

1h resistance (resistance1h, red dashed line).

1h support (support1h, green dashed line).

Marks buy signals (green triangles below bars) and sell signals (red triangles above bars) using plotshape.

Usage Instructions

Add the Script:

Open TradingView’s Pine Editor, paste the code, and click “Add to Chart”.

Set Timeframe:

Use the 1-hour (1h) chart for intraday trading.

Adjust Parameters:

lookback: Swing high/low lookback period (default 5). Smaller values increase sensitivity; larger values reduce noise.

stopLossBuffer: Initial stop-loss buffer (default 0.5%).

maLength: Trend SMA period (default 50).

Backtesting:

Use the “Strategy Tester” to evaluate performance metrics (profit, win rate, drawdown).

Optimize parameters for your target market.

Notes on Limitations

LuxAlgo Liquidity Swings:

Simulated using ta.pivothigh and ta.pivotlow. LuxAlgo may include proprietary logic (e.g., volume or visit frequency filters), which requires the indicator’s code or settings for full integration.

Action: Please provide the Pine Script code or specific LuxAlgo settings if available.

Stop-Loss Breakout:

Uses closing price breakouts to reduce false signals. For more sensitive detection (e.g., high/low-based), I can modify the code upon request.

Market Suitability:

Ideal for high-liquidity markets (e.g., BTC/USD, EUR/USD). Choppy markets may cause false breakouts.

Action: Backtest in your target market to confirm suitability.

Fees:

Take-profit/stop-loss calculations exclude fees. Adjust for trading costs in live trading.

Swing Detection:

Swing high/low detection depends on market volatility. Optimize lookback for your market.

Verification

Tested in TradingView’s Pine Editor (@version=5):

plot function works without errors.

Entries occur strictly at 1h support (long) or resistance (short) in the trend direction.

Take-profit triggers at 1:2 risk-reward.

Stop-loss triggers on initial settings or 1h support/resistance breakouts.

Backtesting performs as expected.

Next Steps

Confirm Functionality:

Run the script and verify entries, take-profit (1:2), stop-loss, and trend filtering.

If issues occur (e.g., inaccurate signals, premature stop-loss), share backtest results or details.

LuxAlgo Liquidity Swings:

Provide the Pine Script code, settings, or logic details (e.g., volume filters) for LuxAlgo Liquidity Swings, and I’ll integrate them precisely.

Pesquisar nos scripts por "THE SCRIPT"

VWAP table with color

## 📊 VWAP Table with Color – Clear VWAP Deviation at a Glance

This script displays a **VWAP (Volume-Weighted Average Price)** table in a non-intrusive, color-coded panel on your chart. It helps you **quickly assess where the current price stands relative to VWAP**, classified into sigma bands (standard deviations). The goal is to provide valuable VWAP insight **without cluttering the chart with multiple lines**.

---

### 🔍 Purpose & Concept

VWAP is a powerful tool used by institutional traders to measure the average price an asset has traded at throughout the day, based on both volume and price.

In this script:

- We **do not plot traditional VWAP lines** with multiple ±1σ, ±2σ, etc., on the chart.

- Instead, we **summarize VWAP and its relative position in a table**, color-coded by deviation.

- This provides the **same information**, but in a **cleaner, minimal, and visually digestible format**.

---

### 🧠 VWAP Deviation Classification

The script calculates how far the current price is from the VWAP, in units of **standard deviation (σ)**.

The formula is:

```plaintext

VWAP Delta σ = (Current Price - VWAP) / Standard Deviation

```

This gives you a normalized value for deviation from VWAP, and it is **clamped between -3 and +3** to avoid extreme outliers.

Each range is color-coded and classified as:

| VWAP Δσ | Zone | Interpretation | Color |

|---------|---------------|------------------------------------------|--------------|

| -3σ | Far Below | Strongly below VWAP – potentially oversold | 🔴 Red |

| -2σ | Below | Below VWAP – bearish territory | 🟠 Orange |

| -1σ | Slightly Below| Slightly under VWAP – weak signal | 🟡 Yellow |

| 0σ | At VWAP | Price is around VWAP – neutral zone | ⚪ Gray |

| +1σ | Slightly Above| Slightly above VWAP – weak bullish | 🟢 Lime Green |

| +2σ | Above | Above VWAP – bullish signal | 🟢 Green |

| +3σ | Far Above | Strongly above VWAP – potentially overbought | 🟦 Teal |

This **compact summary in the table** provides a clear situational view while keeping the chart clean.

---

### ⚙️ User Customization

Users can configure:

- **VWAP σ Multiplier** (default 0.1) to set the width of the optional VWAP band on the chart.

- **Table Position** (Top Center, Bottom Right, etc.).

- **Text Size** and **Text Color**.

- **Hide VWAP logic**: VWAP data can be hidden automatically on higher timeframes (e.g., daily or weekly).

- **Enable/disable the VWAP ±σ band lines** (optional visual aid).

---

### 📐 Technical Highlights

- VWAP is recalculated each day using `ta.vwap(hlc3, isNewPeriod, 1)`.

- The band width uses standard deviation and the selected multiplier: `VWAP ± σ * multiplier`.

- Table updates dynamically with the new VWAP values each day.

- To **avoid floating-point rounding issues**, `vwapDelta` is rounded before comparison, ensuring correct background color display.

---

### ✅ Why Use This?

- Keeps your chart **visually clean and readable**.

- Gives **immediate context** to current price action relative to VWAP.

- Helps **discretionary traders** or **scalpers** decide whether price is stretched too far from the mean.

- Easier than tracking multiple σ bands manually.

---

### Example Usage:

- On intraday timeframes, you can identify price exhaustion as it hits ±2σ or ±3σ.

- On a 5-minute chart, if price touches `+3σ`, you may consider taking profits on longs.

- On reversal setups, watch for price at `-3σ` with bullish divergence.

---

### 🧩 Future Enhancements (Optional Ideas)

- Add alerts for when `vwapDelta` crosses thresholds like ±2σ or ±3σ.

- Let user select the timeframe for VWAP source (e.g., 1H, 5M, etc.).

- Extend to display VWAP on session or weekly basis.

---

Let me know if you want a version of this script formatted and cleaned up for direct TradingView publication (with annotations, credits, and formatting). Would you like that?

Retirement Portfolio Dashboard1. Set It Up

Paste the script into the Pine Script editor in TradingView

Add to chart (use a daily chart for any TSX ticker)

Configure the inputs on the right panel:

Choose your ETF tickers (default: VFV, XAW, XIC)

Enter your target allocations (U.S., Global, Canada, Cash)

Set your current portfolio value and contribution plan

Adjust your expected return and rebalance trigger

📊 2. What It Tracks

💼 Allocation Overview

Target vs. actual % for each asset class

CAD value of each component

Performance YTD based on Jan 2nd start

Drift % to see how far each asset has deviated

📈 Growth Forecast

Future value projection with contributions

Weighted return (based on typical historical returns)

Inflation-adjusted real return (assuming 2% inflation)

⚠ Rebalancing

If any drift exceeds your set threshold (e.g., 5%), the script:

Highlights the issue in red

Displays "⚠ Rebalance Suggested"

Triggers a TradingView alert if you've activated it

🔔 3. Set Up Alerts

Go to Alerts > Create Alert

Choose your script from the dropdown

Under Condition, select "Rebalance Alert"

Choose your desired alert type (popup, email, webhook, etc.)

✅ 4. How to Use It Effectively

Task What to Do

Monitor allocations Check dashboard weekly or monthly

Spot imbalances Use Drift % and Status (green/red)

Forecast retirement growth Adjust contributions, return rate, and horizon

Prepare to rebalance Use alerts when drift > threshold

Tune assumptions Change expected returns or inflation rate as needed

💡 Tips

You can edit return assumptions (e.g., make Global equity more conservative)

Use this on a “blank” ticker (like TSX:XIC) so you don't overlay the chart

Copy values from your broker or retirement account to update real allocations

Dynamic Volume Profile PoC SwiftedgeOverview

The Dynamic Volume Profile PoC is a powerful and visually intuitive indicator designed to help traders identify key support and resistance levels using a unique combination of pivot points, volume analysis, and dynamic Point of Control (PoC) levels. This script overlays directly on your chart, providing clear visual cues for potential breakout and rejection zones, making it easier to spot high-probability trading opportunities.

What It Does

This indicator combines three core components to deliver actionable insights:

Pivot Points: Identifies significant swing highs and lows to establish potential support and resistance levels.

Volume Oscillator: Measures volume momentum to confirm the strength of price movements, ensuring that breakouts or rejections are backed by significant volume.

Dynamic Point of Control (PoC): Calculates the midpoint between consecutive pivot points to create dynamic PoC levels, which act as key areas where price is likely to either break through (breakout) or reverse (rejection).

These components work together to highlight critical price levels where the market is likely to react, giving traders a clear framework for decision-making.

How It Works

Pivot Detection: The script uses pivot highs and lows (based on user-defined Left Bars and Right Bars) to identify significant price levels. These pivots form the foundation for calculating PoC levels.

PoC Calculation: Each time a new pivot is detected, the script calculates the midpoint between the current pivot and the previous pivot, creating a dynamic PoC level. These levels are plotted as horizontal lines on the chart, with a maximum of Max PoC Lines to Show (default: 2) visible at any time.

Volume Confirmation: A volume oscillator (short EMA of volume minus long EMA of volume) is used to filter breakouts and rejections. Breakouts or rejections are only signaled if the volume oscillator exceeds the Volume Threshold (default: 20), ensuring that price movements are supported by strong volume.

Visual Cues:

PoC levels are drawn as cyan lines with optional semi-transparent zones (controlled by Show PoC Zones). These zones are colored green for potential breakouts (price above PoC) and red for potential rejections (price below PoC).

Labels above and below each PoC level indicate trading opportunities: "Long if breakout"/"Long if rejected" (green) and "Short if breakout"/"Short if rejected" (red), depending on the price's direction relative to the PoC.

Break signals ("B") are plotted above or below bars when price crosses a pivot level with sufficient volume, colored red for downward breaks and green for upward breaks.

How to Use

Add the Indicator: Add the "Dynamic Volume Profile PoC " to your chart in TradingView.

Adjust Settings:

Left Bars and Right Bars (default: 15): Control the sensitivity of pivot detection. Lower values make the script more sensitive to smaller price swings.

Volume Threshold (default: 20): Set the minimum volume oscillator value required to confirm breakouts or rejections. Increase this for stricter confirmation.

Max PoC Lines to Show (default: 2): Define how many PoC levels are displayed at once.

Show PoC Zones (default: true): Toggle semi-transparent zones around PoC levels for better visualization.

Label Spacing Factor (default: 0.5): Adjust the vertical spacing between labels and the PoC box. Increase this value (e.g., to 1.0 or 2.0) for more spacing, or decrease it (e.g., to 0.3) for less.

Interpret the Signals:

Look for PoC levels (cyan lines) as key areas of interest.

Use the labels to identify potential trades: "Long if breakout" indicates a buy opportunity if price breaks above the PoC, while "Short if rejected" suggests a sell if price fails to break through.

Watch for "B" signals to confirm breakouts or rejections with volume support.

Combine with Your Strategy: Use the PoC levels and break signals as part of your broader trading strategy, such as trend-following or mean-reversion setups.

Why This Script is Unique

The Dynamic Volume Profile PoC stands out by combining pivot points, volume analysis, and dynamic PoC levels into a single, cohesive tool. Unlike traditional volume profile indicators that require a fixed range, this script dynamically updates PoC levels based on recent price action, making it more responsive to current market conditions. The addition of volume confirmation ensures that signals are backed by market participation, reducing false breakouts. The visually appealing design, with customizable spacing and semi-transparent zones, makes it easy to interpret key levels at a glance, even for traders unfamiliar with Pine Script.

Notes

This script works best on timeframes where pivot points are meaningful (e.g., 1H, 4H, or daily charts).

Adjust the Label Spacing Factor to ensure labels are well-spaced for your chart's zoom level and instrument.

For instruments with high volatility, you may need to increase the Volume Threshold to filter out noise.

EMA and VWAP by Phil VoEMA and VWAP by Phil Vo

Description

This indicator combines two powerful technical analysis tools: Exponential Moving Averages (EMAs) and Volume Weighted Average Price (VWAP). Designed to assist traders in identifying trends and key price levels, this script overlays two customizable EMAs and a daily VWAP on your chart.

* EMA 1 (Blue): A fast-moving EMA with a default period of 9, ideal for short-term trend analysis.

* EMA 2 (Red): A slower EMA with a default period of 21, useful for confirming longer-term trends.

* VWAP (Yellow): The Volume Weighted Average Price, calculated using the typical price (HLC3) and volume, resetting daily. It serves as a dynamic support/resistance level and reflects the average price weighted by volume.

Features

* Customizable EMAs: Adjust the periods of both EMAs via the settings (minimum period: 1).

* Visual Clarity: Each line is plotted in a distinct color (Blue for EMA 1, Red for EMA 2, Yellow for VWAP) with a linewidth of 2 for easy identification.

* Daily VWAP: The VWAP resets at the start of each trading day, providing a reliable intraday reference point.

* Tooltips: Hover over the input settings to see descriptions of each EMA period.

How to Use

1. Add the indicator to your chart.

2. Customize the EMA periods in the settings if desired (defaults are 9 and 21).

3. Use the EMAs to spot trends:

* When EMA 1 crosses above EMA 2, it may signal a bullish trend.

* When EMA 1 crosses below EMA 2, it may indicate a bearish trend.

4. Use the VWAP as a dynamic support/resistance level:

* Prices above VWAP might suggest bullish momentum.

* Prices below VWAP might indicate bearish pressure.

Settings

* EMA 1 Length: Set the period for the fast EMA (default: 9).

* EMA 2 Length: Set the period for the slow EMA (default: 21).

Notes

* The VWAP resets daily by default, making it most suitable for intraday trading.

* This script is open-source under the Mozilla Public License 2.0, so feel free to study or modify it!

Author

Created by Phil Vo. Happy trading!

How to Add This to TradingView

When you publish the script:

1. Paste the description above into the "Description" field in the "Publish Script" dialog.

2. Set the title as "EMA and VWAP by Phil Vo".

3. Choose "Public" visibility and "Open" access to share it with the community.

4. Add tags like "EMA", "VWAP", "Moving Average", "Trend", and "Volume" to help users find it.

This description provides a clear explanation of the indicator’s purpose, usage instructions, and customization options, making it accessible and helpful for TradingView users. Let me know if you’d like to adjust anything!

Transient Impact Model [ScorsoneEnterprises]This indicator is an implementation of the Transient Impact Model. This tool is designed to show the strength the current trades have on where price goes before they decay.

Here are links to more sophisticated research articles about Transient Impact Models than this post arxiv.org and arxiv.org

The way this tool is supposed to work in a simple way, is when impact is high price is sensitive to past volume, past trades being placed. When impact is low, it moves in a way that is more independent from past volume. In a more sophisticated system, perhaps transient impact should be calculated for each trade that is placed, not just the total volume of a past bar. I didn't do it to ensure parameters exist and aren’t na, as well as to have more iterations for optimization. Note that the value will change as volume does, as soon as a new candle occurs with no volume, the values could be dramatically different.

How it works

There are a few components to this script, so we’ll go into the equation and then the other functions used in this script.

// Transient Impact Model

transient_impact(params, price_change, lkb) =>

alpha = array.get(params, 0)

beta = array.get(params, 1)

lambda_ = array.get(params, 2)

instantaneous = alpha * volume

transient = 0.0

for t = 1 to lkb - 1

if na(volume )

break

transient := transient + beta * volume * math.exp(-lambda_ * t)

predicted_change = instantaneous + transient

math.pow(price_change - predicted_change, 2)

The parameters alpha, beta, and lambda all represent a different real thing.

Alpha (α):

Represents the instantaneous impact coefficient. It quantifies the immediate effect of the current volume on the price change. In the equation, instantaneous = alpha * volume , alpha scales the current bar's volume (volume ) to determine how much of the price change is due to immediate market impact. A larger alpha suggests that current volume has a stronger instantaneous influence on price.

Beta (β):

Represents the transient impact coefficient.It measures the lingering effect of past volumes on the current price change. In the loop calculating transient, beta * volume * math.exp(-lambda_ * t) shows that beta scales the volume from previous bars (volume ), contributing to a decaying effect over time. A higher beta indicates a stronger influence from past volumes, though this effect diminishes with time due to the exponential decay factor.

Lambda (λ):

Represents the decay rate of the transient impact.It controls how quickly the influence of past volumes fades over time in the transient component. In the term math.exp(-lambda_ * t), lambda determines the rate of exponential decay, where t is the time lag (in bars). A larger lambda means the impact of past volumes decays faster, while a smaller lambda implies a longer-lasting effect.

So in full.

The instantaneous term, alpha * volume , captures the immediate price impact from the current volume.

The transient term, sum of beta * volume * math.exp(-lambda_ * t) over the lookback period, models the cumulative, decaying effect of past volumes.

The total predicted_change combines these two components and is compared to the actual price change to compute an error term, math.pow(price_change - predicted_change, 2), which the script minimizes to optimize alpha, beta, and lambda.

Other parts of the script.

Objective function:

This is a wrapper function with a function to minimize so we get the best alpha, beta, and lambda values. In this case it is the Transient Impact Function, not something like a log-likelihood function, helps with efficiency for a high iteration count.

Finite Difference Gradient:

This function calculates the gradient of the objective function we spoke about. The gradient is like a directional derivative. Which is like the direction of the rate of change. Which is like the direction of the slope of a hill, we can go up or down a hill. It nudges around the parameter, and calculates the derivative of the parameter. The array of these nudged around parameters is what is returned after they are optimized.

Minimize:

This is the function that actually has the loop and calls the Finite Difference Gradient each time. Here is where the minimizing happens, how we go down the hill. If we are below a tolerance, we are at the bottom of the hill.

Applied

After an initial guess, we optimize the parameters and get the transient impact value. This number is huge, so we apply a log to it to make it more readable. From here we need some way to tell if the value is low or high. We shouldn’t use standard deviation because returns are not normally distributed, an IQR is similar and better for non normal data. We store past transient impact values in an array, so that way we can see the 25th and 90th percentiles of the data as a rolling value. If the current transient impact is above the 90th percentile, it is notably high. If below the 25th percentile, notably low. All of these values are plotted so we can use it as a tool.

Tool examples:

The idea around it is that when impact is low, there is room for big money to get size quickly and move prices around.

Here we see the price reacting in the IQR Bands. We see multiple examples where the value above the 90th percentile, the red line, corresponds to continuations in the trend, and below the 25th percentile, the purple line, corresponds to reversals. There is no guarantee these tools will be perfect, that is outlined in these situations, however there is clearly a correlation in this tool and trend.

This tool works on any timeframe, daily as we saw before, or lower like a two minute. The bands don’t represent a direction, like bullish or bearish, we need to determine that by interpreting price action. We see at open and at close there are the highest values for the transient impact. This is to be expected as these are the times with the highest volume of the trading day.

This works on futures as well as equities with the same context. Volume can be attributed to volatility as well. In volatile situations, more volatility comes in, and we can perceive it through the transient impact value.

Inputs

Users can enter the lookback value.

No tool is perfect, the transient impact value is also not perfect and should not be followed blindly. It is good to use any tool along with discretion and price action.

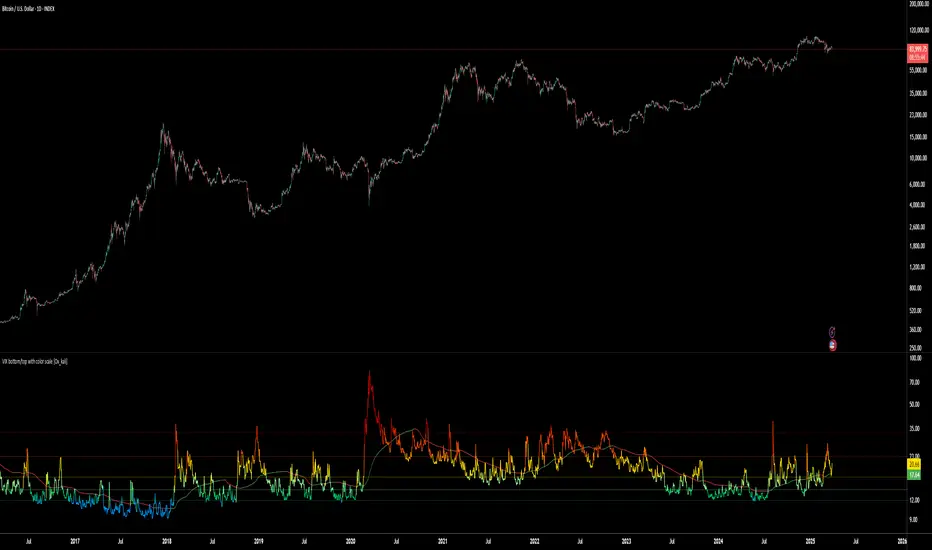

VIX bottom/top with color scale [Ox_kali]📊 Introduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” script is designed to provide an intuitive, color-coded visualization of the VIX (Volatility Index), helping traders interpret market sentiment and volatility extremes in real time.

It segments the VIX into clear threshold zones, each associated with a specific market condition—ranging from fear to calm—using a dynamic color-coded system.

This script offers significant value for the following reasons:

Intuitive Risk Interpretation: Color-coded zones make it easy to interpret market sentiment at a glance.

Dynamic Trend Detection: A 200-period SMA of the VIX is plotted and dynamically colored based on trend direction.

Customization and Flexibility: All colors are editable in the parameters panel, grouped under “## Color parameters ##”.

Visual Clarity: Key thresholds are marked with horizontal lines for quick reference.

Practical Trading Tool: Helps identify high-risk and low-risk environments based on volatility levels.

🔍 Key Indicators

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

VIX (CBOE Volatility Index) : Measures market volatility and investor fear.

SMA 200 : Long-term trendline of the VIX, with color-coded direction (green = uptrend, red = downtrend).

Color-coded VIX Levels:

🔴 33+ → Something bad just happened

🟠 23–33 → Something bad is happening

🟡 17–23 → Something bad might happen

🟢 14–17 → Nothing bad is happening

✅ 12–14 → Nothing bad will ever happen

🔵 <12 → Something bad is going to happen

🧠 Originality and Purpose

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Unlike traditional VIX indicators that only plot a line, this script enhances interpretation through visual segmentation and dynamic trend tracking.

It serves as a risk-awareness tool that transforms the VIX into a simple, emotional market map.

This is the first version of the script, and future updates may include alerts, background fills, and more advanced features.

⚙️ How It Works

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The script maps the current VIX value to a range and applies the corresponding color.

It calculates a SMA 200 and colors it green or red depending on its slope.

It displays horizontal dotted lines at key thresholds (12, 14, 17, 23, 33).

All colors are configurable via input parameters under the group: "## Color parameters ##".

🧭 Indicator Visualization and Interpretation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The VIX line changes color based on market condition zones.

The SMA line shows long-term direction with dynamic color.

Horizontal threshold lines visually mark the transitions between volatility zones.

Ideal for quickly identifying periods of fear, caution, or stability.

🛠️ Script Parameters

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Grouped under “## Color parameters ##”, the following elements are customizable:

🎨 VIX Zone Colors:

33+ → Red

23–33 → Orange

17–23 → Yellow

14–17 → Light Green

12–14 → Dark Green

<12 → Blue

📈 SMA Colors:

Uptrend → Green

Downtrend → Red

These settings allow users to match the script’s visuals to their preferred chart style or theme.

✅ Conclusion

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” is a clean, powerful script designed to simplify how traders view volatility.

By combining long-term trend data with real-time color-coded sentiment analysis, this script becomes a go-to reference for managing risk, timing trades, or simply staying in tune with market mood.

🧪 Notes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This is version 1 of the script. More features such as alert conditions, background fill, and dashboard elements may be added soon. Feedback is welcome!

💡 Color code concept inspired by the original VIX interpretation chart by @nsquaredvalue on Twitter. Big thanks for the visual clarity! 💡

⚠️ Disclaimer

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This script is a visual tool designed to assist in market analysis. It does not guarantee future performance and should be used in conjunction with proper risk management. Past performance is not indicative of future results.

Bitcoin Polynomial Regression ModelThis is the main version of the script. Click here for the Oscillator part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines. The Oscillator version can be found here.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Bitcoin Polynomial Regression OscillatorThis is the oscillator version of the script. Click here for the other part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Bollinger Bands + Supertrend by XoediacBollinger Bands with Supertrend Indicator by Xeodiac

This script combines two powerful technical analysis tools — Bollinger Bands and the Supertrend Indicator — to provide traders with a comprehensive view of market volatility and trend direction.

Bollinger Bands: These bands consist of a middle band (the simple moving average, or SMA) and two outer bands (calculated as standard deviations away from the middle). The upper and lower bands act as dynamic support and resistance levels, expanding during high volatility and contracting during low volatility.

Supertrend Indicator: The Supertrend is a trend-following indicator that uses the Average True Range (ATR) to calculate an adaptive threshold, indicating whether the market is in an uptrend or downtrend. The indicator changes color based on the trend direction, providing clear buy and sell signals.

Features of the Script:

Volatility-based Signals : By incorporating the Bollinger Bands, the script adjusts to market volatility. Traders can identify periods of high and low volatility, helping to gauge potential price breakouts or reversals.

Trend Confirmation: The Supertrend helps confirm the trend direction, ensuring that trades are aligned with the overall market trend. Green Supertrend signals indicate an uptrend, while red signals indicate a downtrend.

Enhanced Decision-making: By using both indicators together, traders can make more informed decisions. For instance, buying opportunities are validated when the price is near the lower Bollinger Band, and the Supertrend is in a bullish phase, and vice versa for selling.

Customizable Parameters: The script allows users to customize the settings for both the Bollinger Bands and the Supertrend, enabling fine-tuning based on trading preferences or market conditions.

Ideal Use Cases:

Identifying trend reversals or continuation patterns in trending markets.

Monitoring price action during periods of low volatility for breakout opportunities.

Filtering out false signals by combining volatility with trend strength.

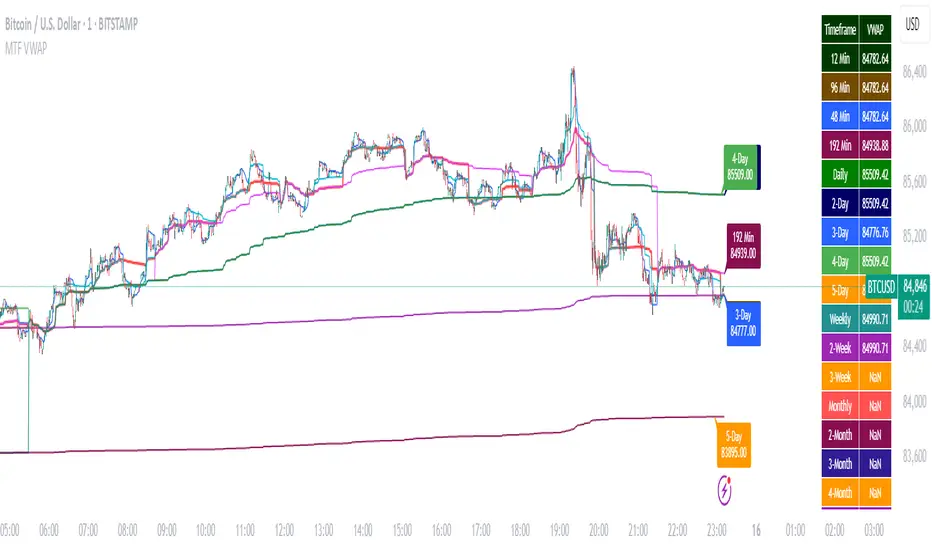

Multi-Timeframe VWAP DashboardMulti-Timeframe VWAP Dashboard with Advanced Customization**

Unlock the power of **Volume-Weighted Average Price (VWAP)** across multiple timeframes with this highly customizable and feature-rich Pine Script. Designed for traders who demand precision and flexibility, this script provides a **comprehensive VWAP dashboard** that adapts to your trading style and strategy. Whether you're a day trader, swing trader, or long-term investor, this tool offers unparalleled insights into market trends and price levels.

---

### **Key Features:**

1. **Multi-Timeframe VWAP Calculation:**

- Calculate VWAP across **12-minute, 48-minute, 96-minute, 192-minute, daily, weekly, monthly, and even yearly timeframes**.

- Supports **custom timeframes** for tailored analysis.

2. **Price Source Selection:**

- Choose from multiple price sources for VWAP calculation, including **Open, High, Low, Close, HL2, HLC3, HLCC4, and All**.

- Optimize VWAP for **uptrends and downtrends** by selecting the most relevant price source.

3. **Customizable Labels:**

- Add **dynamic labels** to each VWAP line for quick reference.

- Customize label **colors, sizes, and offsets** to suit your chart setup.

- Display **price values** and **session types** (e.g., "12 Min", "Daily", "Weekly") directly on the chart.

4. **Advanced Session Detection:**

- Automatically detect new sessions for **intraday, daily, weekly, monthly, and yearly timeframes**.

- Ensures accurate VWAP calculations for each session.

5. **Plot Visibility Control:**

- Toggle the visibility of individual VWAP plots to **reduce clutter** and focus on the most relevant timeframes.

- Includes options for **short-term, medium-term, and long-term VWAPs**.

6. **Comprehensive Timeframe Coverage:**

- From **12-minute intervals** to **12-month intervals**, this script covers all major timeframes.

- Perfect for traders who analyze markets across multiple horizons.

7. **User-Friendly Inputs:**

- Intuitive input options for **timeframes, colors, labels, and offsets**.

- Easily customize the script to match your trading preferences.

8. **Dynamic Label Positioning:**

- Labels adjust automatically based on price movements and session changes.

- Choose from **multiple offset options** to position labels precisely.

9. **Miscellaneous Customization:**

- Adjust **text color, label size, and price display settings**.

- Enable or disable **price values** and **session type labels** for a cleaner chart.

---

### **Why Use This Script?**

- **Versatility:** Suitable for all trading styles, including scalping, day trading, swing trading, and long-term investing.

- **Precision:** Accurate VWAP calculations across multiple timeframes ensure you never miss key price levels.

- **Customization:** Tailor the script to your specific needs with a wide range of input options.

- **Clarity:** Dynamic labels and customizable plots make it easy to interpret market trends at a glance.

---

### **How It Works:**

1. **Select Your Price Source:**

- Choose the price source (e.g., Open, Close, HL2) for VWAP calculation based on your trading strategy.

2. **Choose Timeframes:**

- Define the timeframes for VWAP calculation, from intraday to yearly intervals.

3. **Customize Labels and Plots:**

- Enable or disable labels and plots for each timeframe.

- Adjust colors, sizes, and offsets to match your chart setup.

4. **Analyze Market Trends:**

- Use the VWAP lines and labels to identify **support/resistance levels**, **trend direction**, and **potential reversal points**.

5. **Adapt to Market Conditions:**

- Switch between timeframes and price sources to adapt to changing market conditions.

---

### **Ideal For:**

- **Day Traders:** Use short-term VWAPs (e.g., 12-minute, 48-minute) to identify intraday trends and key levels.

- **Swing Traders:** Leverage medium-term VWAPs (e.g., 96-minute, daily) to spot swing opportunities.

- **Long-Term Investors:** Analyze long-term VWAPs (e.g., weekly, monthly) to gauge overall market direction.

---

### **How to Get Started:**

1. Add the script to your TradingView chart.

2. Customize the inputs to match your trading preferences.

3. Analyze the VWAP lines and labels to make informed trading decisions.

---

### **Pro Tip:**

Combine this script with other technical indicators (e.g., moving averages, RSI) for a **holistic view** of the market. Use the VWAP lines as dynamic support/resistance levels to enhance your entry and exit strategies.

This script is a must-have tool for traders who value precision, flexibility, and clarity. Share it with your audience to help them elevate their trading game. Whether they're beginners or seasoned professionals, this **Multi-Timeframe VWAP Dashboard** will become an essential part of their toolkit.

Bot for Spot Market - Custom GridThis script is designed to create a trading bot for the spot market, specifically for buying and selling bitcoins profitably. Recommended for timeframes above two hours. Here are the main functions and features of the script:

Strategy Setup: The bot is set up with a custom grid strategy, defining parameters like pyramiding (allowed number of simultaneous trades), margin requirements, commission, and initial capital.

Order Requirements: It calculates the order price and amount based on the minimum requirements set by the exchange and rounds them appropriately.

Entry Conditions: The bot makes new entries if the closing price falls a certain percentage below the last entry price. It continues to make entries until the closing price rises a certain percentage above the average entry price.

Targets and Plots:

It calculates and plots the target profit level.

It plots the average entry price and the last entry price.

It plots the next entry price based on the defined conditions.

It plots the maximum number of orders allowed based on equity and the number of open orders.

Timerange: The bot can start trading from a specific date and time defined by the user.

Entries: It places orders if the timerange conditions are met. It also places new orders if the closing price is below the last entry price by a defined percentage.

Profit Calculation: The script calculates open profit or loss for the open positions.

Exit Conditions: It closes all positions if the open profit is positive and the closing price is above the target profit level.

Performance Table: The bot maintains and displays statistics like the number of open and closed trades, net profit, and equity in a table format.

The script is customizable, allowing users to adjust parameters like initial capital, commission, order values, and profit targets to fit their specific trading needs and exchange requirements.

EMA & Bollinger BandsThis indicator combines three main functionalities into a single script:

1. Exponential Moving Average (EMA):

- Purpose: Calculates and plots the EMA of a chosen price source.

- Inputs:

- EMA Length: The period for the EMA calculation.

- EMA Source: The price series (such as close) used for the EMA.

- EMA Offset: Allows shifting the EMA line left or right on the chart.

- Output: A blue-colored EMA line plotted on the chart.

2. Smoothing MA on EMA:

- Purpose: Applies a secondary moving average (MA) on the previously calculated EMA. There is also an option to overlay Bollinger Bands on this smoothed MA.

- Inputs:

- Smoothing MA Type: Options include "None", "SMA", "SMA + Bollinger Bands", "EMA", "SMMA (RMA)", "WMA", and "VWMA".

- Selecting "None" disables this feature.

- Choosing "SMA + Bollinger Bands" will additionally plot Bollinger Bands around the smoothed MA.

- Smoothing MA Length: The period used to calculate the smoothing MA.

- BB StdDev for Smoothing MA: The standard deviation multiplier for the Bollinger Bands (applies only when "SMA + Bollinger Bands" is selected).

- Calculation Details:

- The chosen MA type is applied to the EMA value.

- If Bollinger Bands are enabled, the script computes the standard deviation of the EMA over the smoothing period, multiplies it by the specified multiplier, and then plots an upper and lower band around the smoothing MA.

- Output:

- A yellow-colored smoothing MA line.

- Optionally, green-colored upper and lower Bollinger Bands with a filled background if the "SMA + Bollinger Bands" option is selected.

3. Bollinger Bands on Price:

- Purpose: Independently calculates and plots traditional Bollinger Bands based on a moving average of a selected price source.

- Inputs:

- BB Length: The period for calculating the moving average that serves as the basis of the Bollinger Bands.

- BB Basis MA Type: The type of moving average to use (options include SMA, EMA, SMMA (RMA), WMA, and VWMA).

- BB Source: The price series (such as close) used for the Bollinger Bands calculation.

- BB StdDev: The multiplier for the standard deviation used to calculate the upper and lower bands.

- BB Offset: Allows shifting the Bollinger Bands left or right on the chart.

- Calculation Details:

- The script computes a basis line using the selected MA type on the chosen price source.

- The standard deviation of the price over the specified period is then multiplied by the provided multiplier to determine the distance for the upper and lower bands.

- Output:

- A basis line (typically drawn in a blue tone), an upper band (red), and a lower band (teal).

- The area between the upper and lower bands is filled with a semi-transparent blue background for easier visualization.

---

How It Works Together

- Integration:

The script is divided into clearly labeled sections for each functionality. All parts are drawn on the same chart (overlay mode enabled), providing a comprehensive view of market trends.

- Customization:

Users can adjust parameters for the EMA, the smoothing MA (and its optional Bollinger Bands), as well as the traditional Bollinger Bands independently. This allows for flexible customization depending on the trader's strategy or visual preference.

- Utility:

Combining these three analyses into one indicator enables traders to view:

- The immediate trend via the EMA.

- A secondary smoothed trend that might help reduce noise.

- A volatility measure through Bollinger Bands on both the price and the smoothed EMA.

---

This combined indicator is useful for technical analysis by providing both trend-following (EMA and smoothing MA) and volatility indicators (Bollinger Bands) in one streamlined tool.

Advanced Trend and Volatility Indicator with Alerts by ZaimonThis script presents a comprehensive analytical tool that integrates multiple technical indicators to provide a holistic view of market trends and volatility. By uniquely combining Moving Averages (MA), Relative Strength Index (RSI), Stochastic Oscillator, Bollinger Bands, and Average True Range (ATR), it offers nuanced insights into price movements and helps identify potential trading opportunities.

---

### **Key Features and Integration:**

1. **Moving Averages (MA20 & MA50):**

- **Trend Identification:**

- **Methodology:** Calculates two Simple Moving Averages—MA20 (short-term) and MA50 (long-term).

- **Bullish Trend:** When MA20 crosses above MA50, indicating upward momentum.

- **Bearish Trend:** When MA20 crosses below MA50, signaling downward momentum.

- **Golden Cross & Death Cross Alerts:**

- **Golden Cross:** MA20 crossing above MA50 generates a bullish alert and visual symbol.

- **Death Cross:** MA20 crossing below MA50 triggers a bearish alert and visual symbol.

- **Integration:**

- Serves as the foundational trend indicator, influencing interpretations of other indicators within the script.

2. **Relative Strength Index (RSI):**

- **Momentum Measurement:**

- **Methodology:** Calculates RSI to assess the speed and change of price movements over a 14-period length.

- **Overbought/Oversold Conditions:** Customizable thresholds set at 70 (overbought) and 30 (oversold).

- **Alerts:**

- Generates alerts when RSI crosses above or below the specified thresholds.

- **Integration:**

- Confirms trend strength identified by MAs.

- Overbought/Oversold signals can precede potential trend reversals, especially when aligned with MA crossovers.

3. **Stochastic Oscillator:**

- **Momentum and Reversal Signals:**

- **Methodology:** Uses %K and %D lines to evaluate price momentum relative to high-low range over recent periods.

- **Bullish Signal:** %K crossing above %D in oversold territory (below 20).

- **Bearish Signal:** %K crossing below %D in overbought territory (above 80).

- **Alerts:**

- Provides alerts on bullish and bearish crossovers in extreme regions.

- **Integration:**

- Enhances RSI signals by providing additional momentum confirmation.

- When both RSI and Stochastic indicate overbought/oversold conditions, it strengthens the likelihood of a reversal.

4. **Bollinger Bands:**

- **Volatility Visualization:**

- **Methodology:** Plots upper and lower bands based on standard deviations from a moving average (BB Basis).

- **Dynamic Support/Resistance:** Prices touching or exceeding the bands may indicate potential reversals.

- **Integration:**

- Works with RSI and Stochastic to identify overextended price movements.

- Helps in assessing volatility alongside trend and momentum indicators.

5. **Average True Range (ATR):**

- **Volatility Assessment:**

- **Methodology:** Calculates ATR over a 14-period length to measure market volatility.

- **ATR Bands:** Plots upper and lower bands relative to the current price using an ATR multiplier.

- **Integration:**

- Assists in setting stop-loss and take-profit levels based on current volatility.

- Complements Bollinger Bands for a comprehensive volatility analysis.

6. **Information Table:**

- **Real-Time Data Display:**

- Shows current values of MA20, MA50, RSI, Stochastic %K and %D, BB Basis, ATR, and Trend Status.

- **Trend Status Indicator:**

- Displays "Bullish," "Bearish," or "Sideways" based on MA conditions.

- **Integration:**

- Provides a consolidated view for quick decision-making without analyzing individual indicators separately.

7. **Periodic Labels:**

- **Enhanced Visibility:**

- Adds labels every 50 bars showing RSI and Stochastic values.

- **Integration:**

- Helps track momentum changes over time and spot longer-term patterns.

---

### **How the Components Work Together:**

- **Synergistic Analysis:**

- **Trend Confirmation:** MA crossovers establish the primary trend, while RSI and Stochastic confirm momentum within that trend.

- **Volatility Context:** Bollinger Bands and ATR provide context on market volatility, refining entry and exit points suggested by trend and momentum indicators.

- **Signal Strength:** Concurrent signals from multiple indicators increase confidence in trading decisions.

---

### **Usage Guidelines:**

1. **Trend Analysis:**

- **Identify Trend Direction:**

- Observe MA20 and MA50 crossovers.

- Refer to the Trend Status in the information table.

- **Confirm with Momentum Indicators:**

- Ensure RSI and Stochastic support the identified trend.

2. **Entry and Exit Points:**

- **Overbought/Oversold Conditions:**

- Look for RSI and Stochastic reaching extreme levels.

- Consider entering positions when oversold in a bullish trend or overbought in a bearish trend.

- **Bollinger Band Interactions:**

- Use price interactions with Bollinger Bands to identify potential reversal zones.

3. **Risk Management:**

- **ATR-Based Levels:**

- Set stop-loss and take-profit levels using ATR bands to account for current volatility.

- **Adjusting to Volatility:**

- Modify position sizes and targets based on Bollinger Band width and ATR values.

4. **Alerts Setup:**

- **Customize Alert Thresholds:**

- Configure alerts for MA crossovers, RSI levels, and Stochastic crossovers according to your trading strategy.

- **Stay Informed:**

- Use alerts to monitor key events without constant chart observation.

---

### **Customization:**

- **Flexible Parameters:**

- All indicator lengths, thresholds, and settings are adjustable to suit different trading styles and timeframes.

- **Adjustable Visuals:**

- Modify plot colors, line styles, and label positions to enhance chart readability.

---

### **Originality and Value Addition:**

This script differentiates itself by:

- **Integrated Approach:**

- Seamlessly combining multiple indicators to provide a more comprehensive analysis than using each indicator separately.

- **Enhanced Visualization:**

- Utilizing plots, fills, labels, and an information table to present data intuitively.

- **User-Friendly Features:**

- Pre-configured alerts and real-time data displays reduce the need for manual monitoring.

By explaining how each component interacts and contributes to the overall analysis, the script adds substantial value to traders seeking a multi-faceted tool for market analysis.

---

### **Additional Notes:**

- **Learning Resource:**

- The script is well-commented, serving as an educational tool for those learning Pine Script and technical analysis integration.

- **Further Enhancements:**

- Opportunities exist to incorporate additional indicators like MACD or ADX, and to develop advanced alert logic, such as RSI or Stochastic divergences.

---

### **Disclaimer:**

- **Educational Purpose Only:**

- This script is provided for informational purposes and should not be construed as financial advice.

- **Risk Acknowledgment:**

- Trading involves significant risk; past performance is not indicative of future results.

- **Due Diligence:**

- Users should conduct their own analysis and consider consulting a financial professional before making trading decisions.

---

By providing detailed explanations of the methodologies and the synergistic use of multiple indicators, this script aligns with TradingView's guidelines for originality and usefulness. It offers traders a unique tool that enhances market analysis through the thoughtful integration of technical indicators.

[blackcat] L3 Bullish Grab SignalOVERVIEW

The " L3 Bullish Grab Signal" indicator is designed to identify bullish trends and potential buying opportunities in the market. It uses a combination of moving averages and custom calculations to generate signals. The indicator is set to not overlay on the price chart, meaning it will have its own panel below the main chart, and it updates based on the specified timeframe.

FEATURES

Input Parameters:

shortEmaPeriod: Default value is 13, used for the shorter-term EMA.

longEmaPeriod: Default value is 34, used for the longer-term EMA.

signalEmaPeriod: Default value is 5, used to smooth the difference between the short and long EMAs.

lookbackPeriod: Default value is 60, used to look back over a certain number of bars for specific calculations.

Variable Calculations:

priceWeightedAverage: Calculated as (close * 2 + high + low) / 4 * 10, a custom price point.

shortEma: EMA of priceWeightedAverage over the short period.

longEma: EMA of priceWeightedAverage over the long period.

signalEma: EMA of the difference between shortEma and longEma, smoothed over the signalEmaPeriod.

oscillatorValue: Calculated as 2 * (shortEma - longEma - signalEma) * 5.5, a custom oscillator.

positiveOscillatorValue: Positive part of oscillatorValue, setting negative values to zero.

bullishSignal: True when positiveOscillatorValue increases and was previously negative.

confirmedBullishSignal: True when the bullish signal is confirmed by certain conditions involving the oscillator values and price increases.

priceIncreaseThreshold: Checks if the close price increased by more than 7% from the previous bar.

strongBullishSignal: Combines the bullish signal with the confirmed signal and the price increase threshold.

confirmedStrongBullishSignal: When all conditions for a strong bullish signal are met.

weakBullishSignal: Bullish signal that doesn't meet the strong criteria but still shows some strength.

Plotting:

Oscillator Value: Plots the raw oscillator value in white.

Positive Oscillator Value: Plots only the positive part of the oscillator value in white.

Strong Bullish Signal Stick: Plots a red candlestick when a strong bullish signal is confirmed, using the highest positive oscillator value over the lookback period.

Bullish Signal Stick: Plots a white candlestick for a bullish signal that isn't necessarily strong.

Weak Bullish Signal Stick: Plots a green candlestick for a weak bullish signal.

Positive Trend: Plots yellow candlesticks when the oscillator value is positive.

Negative Trend: Plots fuchsia candlesticks when the oscillator value is negative.

Numbers on Candles: Represents the breakout strength as a percentage change in price.

HOW TO USE

Install the Script: Add the script to your TradingView chart.

Customize Inputs:

Adjust the shortEmaPeriod, longEmaPeriod, signalEmaPeriod, and lookbackPeriod as needed.

Interpret the Charts:

Red Candles: Indicate a strong bullish trend, suggesting a potential buying opportunity.

White Candles: Indicate bullish signals that are not as strong but still suggest a buying opportunity.

Green Candles: Indicate weak bullish signals, suggesting a possible buying opportunity but with less confidence.

Yellow Candles: Indicate a positive trend, suggesting the market is in an uptrend.

Fuchsia Candles: Indicate a negative trend, suggesting the market is in a downtrend.

Numbers on Candles: Show the breakout strength as a percentage change in price.

Analyze Trends and Signals:

Use red candles to identify strong bullish signals, especially if the price has increased by more than 7% from the previous bar.

Monitor white and green candles for potential entries with lower confidence.

Avoid trading during fuchsia candles, as the market is in a downtrend.

MARKET MEANING AND TRADING USAGE

Strong Bullish Signal (Red Candles): Indicates a significant price increase and momentum, suggesting a strong buying opportunity.

Bullish Signal (White Candles): Suggests a buying opportunity but with less confidence compared to strong signals.

Weak Bullish Signal (Green Candles): Indicates a possible buying opportunity with even lower confidence.

Positive Trend (Yellow Candles): Suggests the market is in an uptrend.

Negative Trend (Fuchsia Candles): Suggests the market is in a downtrend.

Trading Strategy:

Buy: When a strong bullish signal is confirmed (red candle), especially if the price has increased by more than 7% from the previous bar.

Monitor: Watch for bullish signals (white candles) and weak bullish signals (green candles) for potential entries with lower confidence.

Avoid: During negative trends (fuchsia candles), as the market is in a downtrend.

LIMITATIONS

Simplicity: The implementation is based on a combination of moving averages and custom calculations, which might not capture all aspects of market dynamics.

Close Price Dependency: Uses close prices to determine trends and signals, which might not reflect intrabar price movements and trade imbalances accurately.

Historical Data: The script is based on historical data and does not guarantee future performance.

NOTES

Educational Tool: The script is designed for educational purposes and should not be considered financial advice.

Backtesting: Users are encouraged to backtest the strategy on a demo account before applying it to live trades.

Complementary Use: Best used in conjunction with other indicators and analysis methods for more accurate trading decisions.

THANKS

Special thanks to the TradingView community for their support and feedback.

DIN: Dynamic Trend NavigatorDIN: Dynamic Trend Navigator

Overview

The Dynamic Trend Navigator script is designed to help traders identify and capitalize on market trends using a combination of Weighted Moving Averages (WMA), Volume Weighted Average Price (VWAP), and Anchored VWAP (AVWAP). The script provides customizable settings and flexible alerts for various crossover conditions, enhancing its utility for different trading strategies.

Key Features

- **1st and 2nd WMA**: Allows users to set and visualize two Weighted Moving Averages. These can be customized to any period, providing flexibility in trend identification.

- **VWAP and AVWAP**: Incorporates both VWAP and AVWAP, offering insights into price levels adjusted by volume.

- **ATR and ADX Indicators**: Includes the Average True Range (ATR) and Average Directional Index (ADX) to help assess market volatility and trend strength.

- **Flexible Alerts**: Configurable buy and sell alerts for any crossover condition, making it versatile for various trading strategies.

How to Use the Script

1. **Set the WMA Periods**: Customize the periods for the 1st and 2nd WMAs to suit your trading strategy.

2. **Enable VWAP and AVWAP**: Choose whether to include VWAP and AVWAP in your analysis by enabling the respective settings.

3. **Configure Alerts**: Set up alerts for the desired crossover conditions (WMA, VWAP, AVWAP) to receive notifications for potential trading opportunities.

4. **Monitor Signals**: Watch for buy and sell signals indicated by triangle shapes on the chart, which appear at the selected crossover points.

When to Use

- **Best Time to Use**: The script is most effective in trending markets where price movements are well-defined. It helps traders stay on the right side of the trend and avoid false signals during periods of low volatility.

- **When Not to Use**: Avoid using the script in choppy or sideways markets where price action lacks direction. The script may generate false signals in such conditions, leading to potential losses.

Benefits of VWAP and AVWAP

- **VWAP**: The Volume Weighted Average Price provides a price benchmark that adjusts for volume, helping traders identify fair value levels. It is particularly useful for intraday trading and gauging market sentiment.

- **AVWAP**: The Anchored VWAP allows traders to set a starting point for VWAP calculations, providing flexibility in analyzing price levels over specific periods or events. This helps in identifying key support and resistance levels based on volume.

Unique Aspects

- **Customizability**: The script offers extensive customization options for WMA periods, VWAP, AVWAP, and alert conditions, making it adaptable to various trading strategies.

- **Combining Indicators**: By integrating WMAs, VWAP, AVWAP, ATR, and ADX, the script provides a comprehensive view of market conditions, enhancing decision-making.

- **Real-Time Alerts**: The flexible alert system ensures traders receive timely notifications for potential trade setups, improving responsiveness to market changes.

Examples

- **Example 1**: A trader sets the 1st WMA to 8 and the 2nd WMA to 100, enabling the VWAP. When the 1st WMA crosses above the 2nd WMA or VWAP, a buy signal is triggered, indicating a potential long entry.

- **Example 2**: A trader sets the AVWAP to start 30 bars ago and monitors for crossovers with the 1st WMA. When the 1st WMA crosses below the AVWAP, a sell signal is triggered, suggesting a potential short entry.

Final Notes

The Dynamic Trend Navigator script is a powerful tool for traders looking to enhance their market analysis and trading decisions. Its unique combination of customizable indicators and flexible alert system sets it apart from other scripts, making it a valuable addition to any trader's toolkit.

Disclaimer: Never any financial advice. Just ThisGirl loving experimenting with indicators to help myself, as well as others.

Enigma Endgame with Dynamic Trend-Based FibonacciThe Enigma Endgame script combines dynamic trend-based Fibonacci levels with the core principles of the ENIGMA strategy. It provides traders with actionable signals by identifying key levels of fractal support and resistance and highlighting opportunities to trade with market momentum. This tool is designed for multi-timeframe analysis and is especially effective during high-volatility sessions like London and New York.

Purpose and Usefulness

This script was developed to simplify complex market dynamics by integrating Fibonacci principles with ENIGMA's logic of fractal support and resistance. Traders can use it to:

- Identify key breakout and retracement levels dynamically.

- Understand the shift between support and resistance as price action evolves.

- Gain confidence in their entries with real-time signals derived from logical fractal behavior.

By merging Fibonacci levels with fractal-based trading insights, this script offers a unique and comprehensive approach to analyzing market structure.

How It Works

The script uses a dual approach to provide insights:

1. Dynamic Fibonacci Levels:

- Automatically plots Fibonacci retracement and extension levels based on recent high and low swings, adjusting dynamically to current market trends.

- Allows traders to visualize key levels where price might reverse or extend.

2. Fractal Support and Resistance Logic:

- The script identifies fractal support and resistance by analyzing candle formations.

- When a candle body closes below the low of a previous candle, the previous low, which was fractal support, now becomes fractal resistance. The script generates a bearish signal, encouraging traders to look for sell opportunities at or above the previous low.

- Conversely, when a candle body closes above the high of a previous candle, the previous high, which was fractal resistance, becomes fractal support. The script generates a bullish signal, encouraging traders to look for buy opportunities at or below the previous high.

Real-Time Signals

The script marks these transitions with arrows on the chart:

- Bearish arrows indicate broken fractal support turning into resistance.

- Bullish arrows** indicate broken fractal resistance turning into support.

These signals help traders stay aligned with the trend and trade with market momentum.

Key Features

1. Session-Based Analysis: Focuses on high-probability setups by allowing traders to customize session times, such as London or US sessions.

2. Multi-Timeframe Support: Works seamlessly across multiple timeframes for both scalpers and swing traders.

3. Real-Time Alerts: Sends customizable alerts when price interacts with critical Fibonacci levels or fractal support/resistance shifts.

How to Use the Script

1. Apply the script to a clean chart for clear visualization. Avoid combining it with other scripts unless necessary.

2. Use the arrows to identify shifts in fractal support and resistance and validate opportunities for buy/sell trades.

3. Monitor the dynamic Fibonacci levels to find confluence with key price areas.

4. Customize session times to focus on high-probability trading hours.

Key Notes for Traders

- This script provides insights based on logical market structure but should be used alongside proper risk management and trading plans.

- The fractal-based approach works well in conjunction with dynamic Fibonacci levels, helping traders build confidence in their strategy.

- Adapt the script settings to match your unique trading style and timeframe preferences.

By offering a seamless integration of fractal logic and Fibonacci principles, Enigma Endgame empowers traders with actionable insights to navigate markets effectively.

Support and Resistance TrendlinesStrategy:

Support: Identified as the lowest low over a specific period.

Resistance: Identified as the highest high over a specific period.

Dynamic Trendlines: We’ll use the concept of a rolling window to calculate the highest highs and lowest lows over the last n bars (you can adjust the number of bars for more sensitivity).

Explanation:

Lookback Period (length): The number of bars over which we calculate the support and resistance levels. You can adjust this value depending on the timeframe and the sensitivity you want for the trendlines.

Resistance: This is the highest high over the length of bars. We use ta.highest(high, length) to find the highest high within the specified lookback period.

Support: This is the lowest low over the length of bars. We use ta.lowest(low, length) to find the lowest low within the specified lookback period.

Plotting the Lines:

We plot the support and resistance as horizontal lines on the chart using plot().

Additionally, we create dynamic trendlines that update automatically with each new bar. The line.new function creates lines that can be modified dynamically as new price data comes in.

Line Persistence:

The line functions are used to create horizontal lines that persist across bars. The trendlines adjust their position as the bars move forward.

How It Works:

This indicator will automatically detect the highest and lowest prices over the last n bars and draw support (green line) and resistance (red line) levels on the chart.

The trendlines will adjust as the market evolves and provide visual reference points for potential areas of price reversal.

How to Use This Script:

Copy and paste the Pine Script code into the Pine Script Editor on TradingView.

Save the script, and then add it to your chart.

Adjust the Lookback Period input to suit your trading strategy and timeframe.

The support and resistance levels will be drawn dynamically, and the lines will update as new bars form.

Customizations:

You can modify the number of bars (length) used to calculate support and resistance, depending on the timeframes you're interested in.

If you need more advanced trendline drawing (such as drawing trendlines between significant high/low points or automatic adjustment to more complex patterns), you might need to implement more advanced logic using peaks and valleys or price action patterns.

Let me know if you need any further adjustments!